Filing ITR for FY 2025-26? Income Tax Department shares 10 mistakes to avoid and tips to follow

Filing ITR for FY 2025-26? Income Tax Department shares 10 mistakes to avoid and tips to follow

Filing ITR for FY 2025-26? Income Tax Department shares 10 mistakes to avoid and tips to follow

Story by Sneha Kulkarni

Filing ITR for FY 2025-26? Income Tax Department shares 10 mistakes to avoid and tips to follow

Before you begin filing your income tax return (ITR) for the Financial Year 2025-26 (Assessment Year 2026-27), you should gather the necessary documents, verify your income details and choose the correct tax regime and ITR form. The Income Tax (I-T) Department has advised taxpayers to file their returns well before the due date to avoid last-minute rush. Here are 10 things to keep in mind before filing your ITR, as advised by the Income Tax Department in a social media post on X (formerly Twitter).

- Choose the correct tax regime

After considering deductions and exemptions available to you, compare tax liability under both regimes and select the appropriate regime that can help you minimise your tax outgo.

- Select the right ITR form

Using the correct ITR form is very important. There are seven types of ITR forms in India. The correct form depends on your residency status, income sources and the total income amount. Note that filing your return using the wrong form may result in the return being treated as defective by the Income Tax Department.

- Check AIS and Form 26AS carefully

Before filing your income tax return, make sure to download and review your Annual Information Statement (AIS) and Form 26AS. Compare the details with your own records. If you notice any mismatch, reconcile it before filing your return.

- Keep all important documents ready

Keeping all your documents handy can make the income tax return filing process much smoother. Keep the following documents ready before you start:

- Form 16 issued by your employer

- Bank statements

- Interest certificates from banks and post offices

- Investment and deduction proofs, wherever applicable

- Details of other income, if any

- These documents will help you report your income accurately.

- Verify pre-filled information

The Income Tax Department provides several details in pre-filled ITR forms. However, do not assume that every detail is correct.

Verify your personal information, including your name, PAN, Aadhaar number, bank account details, email address as well as the mobile number.

Also ensure that your Aadhaar is linked with your PAN card.

- Claim deductions correctly

If you are eligible to claim deductions under the old tax regime or any other applicable provisions, ensure that you enter the correct amounts. Cross-check your investment and expenditure details before submitting the return.

Incorrect reporting of deductions may lead to an additional tax demand or a delay in processing your return.

- Do not provide incorrect information to claim a higher refund

Note that over deductions, under-reporting income or furnishing incorrect details merely to receive a larger tax refund is illegal. Any mismatch may attract scrutiny or notices from the Income Tax Department.

- File your ITR before the due date

It is always better to file returns before the due date. Filing early gives you enough time to correct mistakes, respond to any issues that may arise and avoid last-minute technical glitches.

- Avoid penalties and loss of benefits

Missing the due date may result in a late filing fee, interest on unpaid taxes and, in some cases, the loss of certain tax benefits.

- Complete e-verification after filing

Filing your ITR is not the final step. You must e-verify within the prescribed time limit; otherwise, it will not be treated as a valid return.

Source: The Economic Times.

ITR-7 filing begins: Income Tax Dept launches Excel utility for AY 2026-27; check who can use it

Story by Mohammad Haris

ITR Filing 2026: The income tax department has released the Excel Utility for ITR-7 for Assessment Year (AY) 2026-27, enabling eligible taxpayers to prepare and file their income tax returns offline through the income tax e-filing portal.

“Kind Attention Taxpayers! The Excel Utility for ITR-7 for Assessment Year 2026-27 is now available on the Income Tax e-Filing portal,” Income Tax India said in a post on X on Friday.

ITR-7 is applicable to entities such as charitable and religious trusts, political parties, scientific research associations, universities, educational institutions, hospitals, and other organisations required to file returns under specific provisions of the Income Tax Act.

Taxpayers can download the ITR-7 Excel Utility (Version 1.0) from the Income Tax e-Filing portal, fill in the required details offline, validate the data, generate the JSON file, and upload it on the portal to complete the return filing process.

The latest release follows the phased rollout of income tax return utilities for AY 2026-27, with the department gradually making offline filing tools available for different ITR forms.

What Is the Last Date To File ITR 2026?

Even as the income tax department has enabled ITR-1, ITR-2, ITR-3, ITR-4 and ITR-5 forms for the assessment year 2026-27 (financial year 2025-26), the due dates for the income tax return filing this year are July 31 for individual taxpayers, August 31 for non-audit business cases, and October 31 for business cases that require audit.

The deadline for businesses that require transfer pricing reports (international transactions or specified domestic transactions) is November 30, 2026.

Under which Act will the ITR for income earned during FY 2025-26 be filed?

The ITR for income earned during FY 2025-26 will be filed for the assessment year 2026 -27 under the provisions of the Income Tax Act, 1961. Even though the filing will typically occur after April 1, 2026 (i.e., after the new Income Tax Act, 2025, has come into force), the return relates to a tax year beginning before April 1, 2026, and is therefore governed entirely by the old Act, the income tax department has said.

ITR filing: Don't let one small mistake cost you your tax refund; check these points

©The Economic Times

Filing your Income Tax Return sounds simple, until a small slip turns into a notice, a delayed refund, or an unexpected tax bill. Here's exactly what to double-check before you hit submit this year.

With the ITR filing season underway, the Income Tax Department has shared a simple checklist to help taxpayers file their returns correctly. In a post on X, the department urged taxpayers to prepare well in advance and avoid waiting until the last minute.

"A smooth ITR filing experience begins with the right preparation. Follow these Golden Rules to file your Income Tax Return (ITR) for AY 2026-27 accurately and confidently. Filing your ITR well before the due date can help you avoid unnecessary delays and last-minute rush," the department said.

Income Tax Department's 7 golden rules for ITR filing

CHOOSE THE RIGHT TAX REGIME AND ITR FORM

The department advises taxpayers to first decide whether the old tax regime or the new tax regime is more suitable for them.

It also stresses the importance of selecting the correct ITR form. Filing the wrong return form can lead to complications and delays in processing.

MATCH YOUR INCOME DETAILS BEFORE FILING

Before submitting the return, taxpayers should download their Annual Information Statement (AIS) and Form 26AS from the Income Tax portal.

These documents help verify details such as TDS, TCS and taxes already paid. If there is any mismatch, taxpayers should contact their bank, employer or the concerned deductor and get the records corrected before filing the return.

KEEP ALL IMPORTANT DOCUMENTS READY

The department also advises taxpayers to keep all necessary financial documents handy before they start filing.

These include Form 16, bank statements, interest certificates and investment proofs. Reviewing these documents carefully helps ensure that no income or eligible deduction is missed.

CHECK PRE-FILLED INFORMATION CAREFULLY

Even if the return is pre-filled, taxpayers should not assume every detail is correct.

The department recommends verifying important information such as PAN, address and bank account details. Even a small error can lead to correction requests or delays in processing the return.

Taxpayers should also ensure that the mobile number and email ID mentioned in the return belong to them and are active. The department recommends using the mobile number linked with Aadhaar so that all official communications are received without any issues.

ENTER DEDUCTION DETAILS CORRECTLY

The Income Tax Department has reminded taxpayers to fill in deduction and exemption details accurately.

This includes providing the correct bank details, account numbers and claim amounts wherever required. The responsibility of entering the correct information rests with the taxpayer.

The department also cautioned taxpayers against believing unrealistic promises of higher tax refunds. Even if a tax professional prepares the return, taxpayers should review all the details themselves before submitting it.

DON'T WAIT UNTIL THE DEADLINE

The department has once again urged taxpayers to file their ITR well before the due date instead of waiting until the last few days.

Late filing may attract a late fee. It can also result in the loss of certain deductions and prevent taxpayers from carrying forward eligible losses.

DON'T FORGET TO E-VERIFY YOUR RETURN

Filing the return is only one part of the process. The department has reminded taxpayers to complete e-verification after submitting their ITR.

Those who choose physical verification must send the signed ITR-V to the Centralised Processing Centre (CPC) in Bengaluru by Speed Post within 30 days.

In other words, the Income Tax Department's message is simple, i.e., preparing in advance can help avoid unnecessary errors and delays. Choosing the right tax regime and ITR form, checking income details, verifying pre-filled information and completing e-verification are some of the key steps that can make the ITR filing process smoother for AY 2026-27.

ITR filing 2026: 10 situations where you cannot use ITR-1 and must choose another income tax return form

ITR Filing 2026: ITR-1 Is Not for Everyone—Know When ITR-2, ITR-3 or ITR-4 Becomes Mandatory

Filing an Income Tax Return (ITR) is more than just meeting the tax deadline—it also requires selecting the correct return form based on your income sources and financial transactions. While ITR-1 (Sahaj) is the most commonly used form by salaried employees and pensioners, it is not suitable for every taxpayer.

Tax professionals caution that choosing the wrong ITR form can result in your return being treated as defective by the Income Tax Department, leading to delays in processing or the need to submit a revised return. Therefore, before filing your tax return for the assessment year, it is important to understand whether you are eligible to use ITR-1 or if another form such as ITR-2, ITR-3, or ITR-4 is required.

Here are the key situations where taxpayers should avoid filing ITR-1.

- You Earned Short-Term Capital Gains From Shares or Equity Mutual Funds

If you sold listed shares or equity mutual funds during the financial year and earned Short-Term Capital Gains (STCG), ITR-1 cannot be used.

In most cases, taxpayers reporting such capital gains are required to file ITR-2. However, if your share transactions are treated as business income—such as frequent trading, intraday trading, or derivatives (F&O)—you may need to file ITR-3 instead.

- Long-Term Capital Gains Exceed ₹1.25 Lakh

Taxpayers who have earned Long-Term Capital Gains (LTCG) exceeding ₹1.25 lakh from listed equity shares or equity-oriented mutual funds under Section 112A are not eligible to use ITR-1.

Such capital gains must be reported using the appropriate return form, generally ITR-2.

- You Sold Property or Other Capital Assets

If you sold assets such as:

- Residential or commercial property

- Land

- Gold or jewellery

- Debt mutual funds

- Any other capital asset

the resulting capital gains cannot be disclosed through ITR-1. In these cases, taxpayers should choose a form that allows reporting of capital gains, such as ITR-2 or ITR-3, depending on their overall income profile.

- You Have Business or Professional Income

Individuals earning income from:

- Business operations

- Freelancing

- Consultancy services

- Professional practice

- Proprietorship businesses

cannot file ITR-1.

Generally, such taxpayers are required to file ITR-3. Those opting for the Presumptive Taxation Scheme under the Income Tax Act may instead be eligible to file ITR-4, depending on the nature of their business.

- You Trade in F&O or Intraday Stocks

Income generated through:

- Futures & Options (F&O)

- Intraday equity trading

- Other trading activities classified as business income

cannot be reported in ITR-1.

Since these activities are considered business income under tax laws, the appropriate return form is usually ITR-3.

- You Held Unlisted Equity Shares

If you owned unlisted equity shares at any point during the previous financial year, you are not eligible to use ITR-1.

The Income Tax Department requires additional disclosures for such investments, making ITR-2 or ITR-3 the applicable return forms.

- You Are a Director in a Company

Individuals serving as directors in any company must use return forms that capture director-related disclosures.

As a result, company directors cannot file ITR-1 and are generally required to submit either ITR-2 or ITR-3.

- You Own Foreign Assets or Have Authority Over Overseas Bank Accounts

ITR-1 is not applicable if you:

- Own property outside India

- Hold financial assets abroad

- Have signing authority over a foreign bank account

Foreign asset reporting requires additional schedules that are unavailable in ITR-1.

- You Receive Income From Outside India

If you receive any foreign income, including:

- Salary

- Dividend

- Interest

- Rental income

- Capital gains

ITR-1 cannot be used.

Such taxpayers must report foreign income and applicable disclosures through ITR-2 or ITR-3, depending on the nature of their earnings.

- Your Taxable Income Exceeds ₹50 Lakh or You Have Special Income

You are not eligible to file ITR-1 if:

- Your total taxable income exceeds ₹50 lakh

- You wish to carry forward previous years' losses

- You have income from lotteries, horse racing, or other specified categories

These situations require more detailed disclosures than those available in ITR-1.

What Happens If You Choose the Wrong ITR Form?

Selecting the wrong return form can create unnecessary complications during tax filing.

If the Income Tax Department finds that an incorrect form has been used, it may issue a Defective Return Notice. This can delay the processing of your return, postpone your refund (if applicable), and require you to submit a revised return using the correct form.

Tax experts recommend reviewing all sources of income—including salary, investments, capital gains, business income, and foreign assets—before deciding which ITR form to use.

Choose the Correct Return Form Before Filing

Although ITR-1 remains the simplest option for many salaried individuals and pensioners, it is designed only for taxpayers who meet specific eligibility conditions. The moment your income includes capital gains, business income, foreign assets, overseas earnings, or other complex financial transactions, you may need to switch to ITR-2, ITR-3, or ITR-4.

Choosing the correct form from the outset can help ensure faster processing, avoid notices from the Income Tax Department, and make your tax filing experience smoother.

ITR filing checklist: Keep these documents and details ready before filing income tax return

Filing an Income Tax Return (ITR) is more than just a yearly compliance exercise. So, before filing ITR, taxpayers should first ensure that core identity and banking details are updated and accurate. PAN and Aadhaar must be linked, bank accounts should be pre-validated for refunds, and taxpayers should keep the previous year’s ITR copy handy for reference.

“It is important to have access to e-verification methods such as Aadhaar OTP, net banking or digital signature certificate (DSC) to complete the filing process seamlessly,” said Preeti Gupta, Director at Deloitte.

Here is the checklist of financial documents and tax-related records that one must keep ready beforehand.

AIS, Form 26AS and Form 16 should be reviewed carefully

Apart from identity details, taxpayers should carefully review all tax-related documents before starting the filing process. “Taxpayers should review their Form 16, AIS, TIS and Form 26AS statements and other financial records while preparing the ITR form. These help in selection of the tax regime to be adopted during the year,” said Deepashree Shetty, Partner, Global Mobility Services, Tax & Regulatory Advisory at BDO India.

Choosing between the old and new tax regime

Choosing the correct tax regime is another important decision taxpayers should make before filing returns. The new tax regime, which is now the default system, offers lower tax slab rates but restricts most exemptions and deductions. On the other hand, the old tax regime allows taxpayers to claim benefits such as House Rent Allowance (HRA), Leave Travel Allowance (LTA), deductions under Section 80C, health insurance under Section 80D and home loan interest benefits. Tax experts suggest calculating tax liability under both systems before making a final choice.

Salary, pension and exemption-related documents to keep ready

Income-related documentation should also be organised based on the nature of earnings during the financial year. Salaried employees should keep salary slips, Form 16 and documents supporting exemptions such as rent receipts for HRA claims or travel bills for LTA claims. Pensioners should maintain pension statements and details of annuity income, if any.

Keeping these records ready helps taxpayers accurately report taxable and exempt portions of income while also avoiding errors during reconciliation.

House property and home loan documents

Taxpayers earning rental income should maintain rent agreements, municipal tax receipts and home loan interest certificates. In the case of home loans, the interest and principal repayment components are important not only for deduction claims but also for correctly reporting house property income.

Those claiming HRA should also ensure rent receipts and landlord details are properly maintained, particularly in cases where higher exemption claims are being made.

Capital gains reporting needs detailed records

Investors reporting capital gains must maintain detailed records of share transactions, mutual fund statements and property sale or purchase documents. Proper documentation becomes particularly important after the revised capital gains taxation rules and holding period changes introduced in recent years.

Business and professional income records are equally important

For freelancers, consultants and business owners, maintaining accurate books of accounts, invoices, expense records, GST returns and audit reports, where applicable, is critical. Mismatches between GST filings and ITR disclosures can invite departmental queries.

Professionals opting for presumptive taxation schemes should also verify turnover declarations and eligible deductions before filing returns.

Don’t ignore interest, dividend and other small income sources

Taxpayers should also collect supporting documents for income earned from other sources, such as savings account interest, fixed deposit interest, dividends, commission income or royalty receipts.

Why foreign assets and overseas income must be disclosed

Foreign income and overseas assets require special attention while filing returns. Even if there is no capital gain or active income generated from a foreign bank account, foreign stocks or overseas investments, Indian residents may still need to disclose these holdings in their ITR schedules.

Non-disclosure of foreign assets can attract penalties under the Black Money Act and may also trigger scrutiny from tax authorities. Tax experts advise resident taxpayers to maintain complete details of overseas bank accounts, foreign equity holdings, ESOPs, crypto assets held abroad and foreign income disclosures, wherever applicable.

An income tax refund is issued when the tax paid by a taxpayer during a financial year exceeds the actual tax liability. Excess tax may have been paid through Tax Deducted at Source (TDS), Tax Collected at Source (TCS), or advance tax. Taxpayers can claim the excess amount by filing their Income Tax Return (ITR). After filing the return, the refund status can be tracked online through the income tax e-filing portal and other available channels.

“Taxpayers should carefully review all available exemptions and deductions applicable to them, compare the benefits under both tax regimes, and verify that information reported in tax documents aligns with official records. Even small discrepancies can delay refunds or lead to avoidable notices," said Chandni Anandan, Tax Expert at ClearTax.

A well-prepared return that is complete, accurate, and promptly verified not only improves the likelihood of receiving the correct refund but also makes the filing experience significantly smoother,” added Anandan.

Strategies to maximise tax refund

To maximise an income tax refund, taxpayers should first compare their tax liability under both the old and new tax regimes before filing the return. Selecting the regime that results in the lower tax outgo can significantly increase the refund amount where excess TDS has already been deducted during the year.

Under the old tax regime, taxpayers can reduce taxable income through various deductions. Investments in instruments such as PPF, ELSS, EPF, NSC, life insurance premiums and 5-year tax-saving fixed deposits qualify for deductions of up to Rs 1.5 lakh under Section 80C. Additional tax savings can be claimed through health insurance premiums under Section 80D, where deductions range from Rs 25,000 to Rs 50,000 depending on the age of the insured and family members covered.

Salaried individuals can further reduce their tax liability by claiming House Rent Allowance (HRA) exemption, subject to prescribed conditions, and deduction of up to Rs 2 lakh on interest paid for a self-occupied home loan under Section 24(b). Those contributing to the National Pension System (NPS) can claim an additional deduction of up to Rs 50,000 under Section 80CCD(1B), over and above the Section 80C limit.

Employer contributions to NPS can also provide tax benefits under Section 80CCD(2). This deduction is available under both tax regimes and can be claimed on employer contributions of up to 10 percent of salary under the old regime and up to 14 percent under the new regime, depending on the employer category.

Salaried taxpayers are also entitled to the standard deduction, which is automatically available while computing taxable income. The deduction is Rs 50,000 under the old regime and Rs 75,000 under the new regime. Eligible taxpayers can also benefit from the rebate under Section 87A, which can reduce tax liability to nil if taxable income remains within the prescribed threshold.

Family pension recipients can claim a deduction under Section 57(iia). The deduction available is up to Rs 15,000 under the old regime and up to Rs 25,000 under the new regime, helping reduce taxable income and improve refund eligibility.

How to claim an income tax refund

Filing an Income Tax Return (ITR) is mandatory to claim a refund, even if a taxpayer is not otherwise required to file a return. Once income details and taxes already paid through TDS, TCS, or advance tax are reported, the tax filing utility automatically computes the actual tax liability and any refund due. If the taxes paid exceed the final tax liability, the excess amount is processed as a refund.

Select the correct ITR form: Choose the appropriate ITR form based on factors such as income sources, residential status, and taxpayer category. Filing under an incorrect form can lead to reporting errors, compliance issues, delays in return processing, and slower refund issuance.

Calculate and report income accurately: Ensure that all sources of income, eligible deductions, and exemptions are disclosed correctly to arrive at the right tax liability.

Verify TDS details: Cross-check the TDS information pre-filled in the return with Form 16, Form 16A, or other relevant records to ensure there are no discrepancies.

Provide correct bank account details: Enter accurate and active bank account information, as refunds are credited directly to the bank account linked with the return. Incorrect details may result in delays or failed refund transfers.

Complete e-verification promptly: After filing the return, e-verify it at the earliest. A return is processed only after verification, and timely e-verification helps speed up both return processing and refund issuance.

Source: money Control, LiveMint, Economic Times

Income Tax Slabs – FY 2017-18 (AY-2018-19) and FY 2016-17

Income Tax Slabs for FY 2017-18 (AY 2018-19) and FY 2016-17 (AY 2017-18)

Given below are the rates at which income is taxed in India for income earned in different slabs, and through various heads of income.

The tax rates and Tax Slabs have been arranged depending on the profile and category of the taxpayer / tax paying entity.

New Income Tax Slab Rates for FY 2017-18 (AY 2018-19) - Budget 2017

The Finance Minister also announced that income tax for small companies with an annual turnover of Rs.50 crore would be reduced. Income tax has been reduced to 25% from the previous rate of 30%. It was also announced that all individuals who earn less than Rs.5 lakh per year will have to file a one page I-T return form. The revised tax rates are as given below –

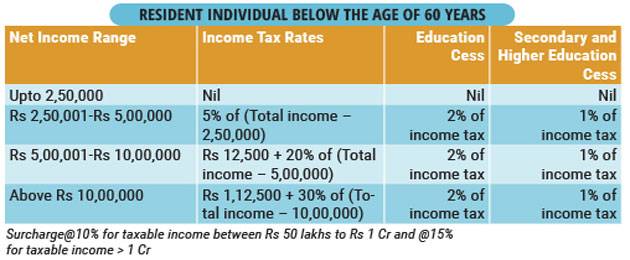

Income tax slab for individual tax payers & HUF (less than 60 years old) (both men & women)

|

Income Tax Slab |

Tax Rate |

|

Income up to Rs. 2,50,000* |

No Tax |

|

Income from Rs. 2,50,000 – Rs. 5,00,000 |

5% |

|

Income from Rs. 5,00,000 – 10,00,000 |

20% |

|

Income more than Rs. 10,00,000 |

30% |

|

Surcharge: 10% of income tax, where total income is between Rs. 50 lakhs and Rs.1 crore. 15% of income tax, where total income exceeds Rs. 1 crore. |

|

|

Cess: 3% on total of income tax + surcharge. |

|

|

* Income upto Rs. 2,50,000 is exempt from tax if you are less than 60 years old. |

|

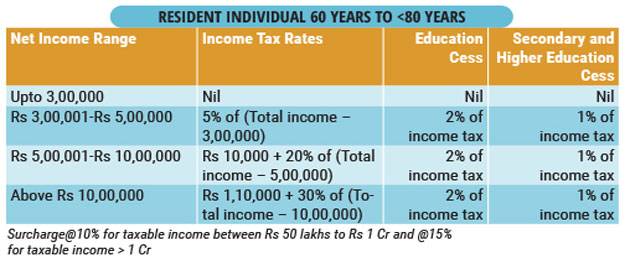

Income tax slab for individual tax payers & HUF (60 years old or more but less than 80 years old) (both men & women)

|

Income Tax Slab |

Tax Rate |

|

Income up to Rs. 3,00,000* |

No Tax |

|

Income from Rs. 3,00,000 – Rs. 5,00,000 |

5% |

|

Income from Rs. 5,00,000 – 10,00,000 |

20% |

|

Income more than Rs. 10,00,000 |

30% |

|

Surcharge: 10% of income tax, where total income is between Rs. 50 lakhs and Rs.1 crore. 15% of income tax, where total income exceeds Rs.1 crore. |

|

|

Cess: 3% on total of income tax + surcharge. |

|

|

* Income up to Rs. 3,00,000 is exempt from tax if you are more than 60 years but less than 80 years of age. |

|

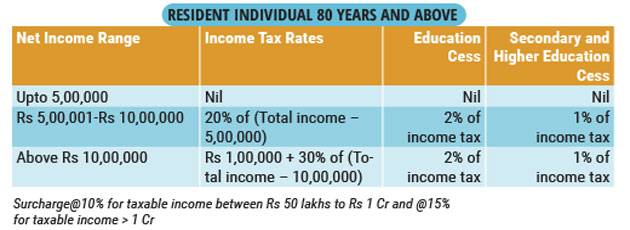

Income tax slab for super senior citizens (80 years old or more) (both men & women)

|

Income Tax Slab |

Tax Rate |

|

Income up to Rs. 2,50,000* |

No Tax |

|

Income up to Rs. 5,00,000* |

No Tax |

|

Income from Rs. 5,00,000 – 10,00,000 |

20% |

|

Income more than Rs. 10,00,000 |

30% |

|

Surcharge: 10% of income tax, where total income is between Rs. 50 lakhs and Rs.1 crore. 15% of income tax, where total income exceeds Rs.1 crore. |

|

|

Cess: 3% on total of income tax + surcharge. |

|

|

*Income up to Rs. 5,00,000 is exempt from tax if you are more than 80 years old. |

|

Customers should note that the Income Tax Exemption limit per FA 2016 is up to a maximum of Rs.2,50,000 for all individuals and HUF other than those who are covered in Part(II) or Part(III).

Below, you Can find a few tables that list out

Income Tax Slab Rates for FY 2016-17 (AY 2017-18)

These income tax slab rates are also applicable for :

* FY 2015-16 (AY 2016-17)

* FY 2014-15 (AY 2015-16)

- Income Tax Slab for Individual Tax Payers :

|

Income Tax Slab |

Rate |

|

Up to Rs.2,50,000 |

No tax |

|

Rs.2,50,000 to Rs.5,00,000 |

10% |

|

Rs.5,00,000 to Rs.10,00,000 |

20% |

|

Over Rs.10,00,000 |

30% |

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 12% of income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

Less:

- Rebate under Section 87A:For individuals with total income less than Rs.5,00,000 – a total rebate amount of Rs.2,000 or 100% of the income tax (whichever is lesser).

- Income Tax Slab for Hindu Undivided Families (HUF) :

|

Income Tax Slab |

Rate |

|

Up to Rs.2,50,000 |

No tax |

|

Rs.2,50,000 to Rs.5,00,000 |

10% |

|

Rs.5,00,000 to Rs.10,00,000 |

20% |

|

Over Rs.10,00,000 |

30% |

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 12% of income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

Less:

- Rebate under Section 87A:For HUFs with total income less than Rs.5,00,000 – a total rebate amount of Rs.2,000 or 100% of the income tax (whichever is lesser).

- Income Tax Slab for legal Entities Registered as Associations of Persons :

|

Income Tax Slab |

Rate |

|

Up to Rs.2,50,000 |

No tax |

|

Rs.2,50,000 to Rs.5,00,000 |

10% |

|

Rs.5,00,000 to Rs.10,00,000 |

20% |

|

Over Rs.10,00,000 |

30% |

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 12% of income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

Less:

- Rebate under Section 87A:For Associations of Persons with total income less than Rs.5,00,000 – a total rebate amount of Rs.2,000 or 100% of the income tax (whichever is lesser).

- Income Tax Slab for Legal Entities Registered as Bodies of Individuals :

|

Income Tax Slab |

Rate |

|

Up to Rs.2,50,000 |

No tax |

|

Rs.2,50,000 to Rs.5,00,000 |

10% |

|

Rs.5,00,000 to Rs.10,00,000 |

20% |

|

Over Rs.10,00,000 |

30% |

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 12% of income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

Less:

- Rebate under Section 87A:For Bodies of Individuals with total income less than Rs.5,00,000 – a total rebate amount of Rs.2,000 or 100% of the income tax (whichever is lesser).

- Income Tax Slab for Other Artificial Judicial Persons :

|

Income Tax Slab |

Rate |

|

Up to Rs.2,50,000 |

No tax |

|

Rs.2,50,000 to Rs.5,00,000 |

10% |

|

Rs.5,00,000 to Rs.10,00,000 |

20% |

|

Over Rs.10,00,000 |

30% |

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 12% of income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

Less:

- Rebate under Section 87A:For Judicial entities with total income less than Rs.5,00,000 – a total rebate amount of Rs.2,000 or 100% of the income tax (whichever is lesser).

- For Resident Senior Citizens (Over the Age of 60, and Under the Age of 80 on the last day of the Previous Year) :

|

Income Tax Slab |

Rate |

|

Up to Rs.3,00,000 |

No tax |

|

Rs.3,00,000 to Rs.5,00,000 |

10% |

|

Rs.5,00,000 to Rs.10,00,000 |

20% |

|

Over Rs.10,00,000 |

30% |

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 12% of income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

Less:

- Rebate under Section 87A:For Resident Indian Senior Citizen taxpayers with total income less than Rs.5,00,000 – a total rebate amount of Rs.2,000 or 100% of the income tax (whichever is lesser).

- For Resident Super Senior Citizens (who are over the age of 80 as on the last day of the Previous Year) :

|

Income Tax Slab |

Rate |

|

Up to Rs.5,00,000 |

No tax |

|

Rs.5,00,000 to Rs.10,00,000 |

20% |

|

Over Rs.10,00,000 |

30% |

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 12% of income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

- For Partnership Firms:

Partnership Firms and LLPs (Limited Liability Partnerships) are to be taxed at the rate of 30%.

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 12% of income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

- For Local Authorities :

Local Authorities are to be taxed at the rate of 30%.

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 12% of income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

- For Domestic Companies :

Domestic Companies are to be taxed at the rate of 30%.

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 7% of the income tax amount. If income is greater than Rs.10,00,00,000 – 12% of the income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

- For Foreign Companies :

|

Nature |

Rate |

|

If the income received by the Foreign Company is in the form of royalties paid by the Indian Government in relation to agreements made with an Indian concern (after March 31st, 1961, and before April 1st, 1976) |

50% |

|

If the income received is in the form of fees for technical services rendered for agreements made with Indian concerns (after February 29th, 1964, and before April 1st, 1976) |

50% |

|

Any other income |

40% |

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 2% of the income tax amount. If income is greater than Rs.10,00,00,000 – 5% of the income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

- For Co-operative Societies :

|

Income Tax Slab |

Rate |

|

Up to Rs.10,000 |

10% |

|

Rs.10,000 to Rs.20,000 |

20% |

|

Over Rs.20,000 |

30% |

Plus:

- Surcharge:If income is greater than Rs.1,00,00,000 – 12% of income tax amount. Subject to marginal relief.

- Education Cess:2% extra – charged on the amount of income tax + surcharge being paid.

- Secondary and Higher Education Cess:1% extra – charged on the amount of income tax + surcharge being paid.

ITR filing for FY 2017-18: Common mistakes that may get you a tax notice – Innocent mistakes Honest taxpayers usually make

A taxpayer should start the ITR filing process by choosing the right form. Income tax experts warn against claiming deductions one is not eligible for.

The due date for filing of income tax return (ITR) for the financial year 2017-18 (assessment year 2018-19) is 31 July 2018. In a rush to meet the deadline, many taxpayers might end up making mistakes which might fetch them a notice from income tax authorities. “Though mistakes committed in ITR filing can be rectified by filing revised return, it would require extra time and efforts,” said Vishal Raheja, assistant manager at Taxmann, an online publisher on taxation and corporate laws.

Income tax return for the assessment year 2018-19 can be revised by 31 March 2019.

The income tax department has notified seven ITR forms for filing of return for FY 2017-18. ITR filing process starts from choosing the correct form, which depends on the nature of income and the status of the taxpayers. Some of the common mistakes that you should avoid committing during ITR filing:

(1) “Don’t presume that if tax has already been paid, you don’t need to file the return,” says Vishal Raheja of Taxmann. If you are resident in India, irrespective of tax liability, you have to file ITR if taxable income exceeds basic exemption limit, which is ₹ 3 lakh for senior citizens (age above 60 years), ₹ 5 lakh for super-senior citizens (above 80 years) and ₹ 2.5 lakh for all other individual taxpayers.

(2) If you choose the wrong ITR form, you may not report the complete information and the income tax department can issue a notice for under-reporting income.

3) However small the income may be, you should report it in our ITR, say tax experts. “Income tax department gets regular information from banks and financial institutions about your transactions which are reconciled with your ITR. If some tax has been deducted from your income but you don’t report the corresponding income in ITR, you might get a notice,” says Raheja.

(4) If you have changed jobs during the year, you have to report income earned from all the employers in your tax return. Further, “if any income of your minor child or spouse is required to be clubbed with your income then you have to report it,” he adds.

(5) Tax experts warn against claiming deductions in ITR for which you are not eligible for. “Some taxpayers claim fake deductions or inflate existing deductions to reduce their income tax liability or to claim refunds,” says Raheja.

(6) A taxpayer should also ensure that ITR data is in sync with that of Form 26AS. In case of any discrepancy, the income tax department could issue notice, seeking explanation for discrepancies in the figures of income or TDS appearing in Form 26AS and income tax return. Form 26AS is basically a consolidated tax credit statement that has all details of various taxes deducted on your income at source. Form 26AS can be accessed from the tax department’s website.

(7) If you are filing ITR belatedly, then make sure that pay late filing fees before filing of ITR, say tax experts. “A late filing fees of ₹ 5,000 shall be charged if the return is filed between 01.08.2018 and 31.12.2018. The fees shall be ₹ 10,000 if return is filed between 01.01.2019 and 31.03.2019. The late filing shall be ₹ 1,000 for small taxpayers whose taxable income is up to ₹ 5 lakh,” says Raheja.

(8) If you fail to either e-verify your ITR or post it to Centralized Processing Centre (CPC) of the income tax department in Bengaluru, return will be treated as an invalid return. While filing ITR you are asked to digitally sign or e-verify it. In case, you do not e-verify your return, you can sign the acknowledgement copy of ITR and post it to CPC, Bangaluru. The acknowledgement has to be sent within 120 days of filing of the return.

1. Not reporting interest income

Though interest earned from fixed deposits, recurring deposits, even tax-saving bank deposits and infrastructure bonds, is fully taxable, people often do not report any interest income below Rs 10,000. The exemption of Rs 10,000 a year under Section 80TTA applies only to the interest earned on the balance in a savings bank account. Even so, you are supposed to declare it in ITR and then claim the deduction. Please click on the following link for Sec. 80TTA : " Deduction under Section 80TTa – Interest on Savings Account"

Another common misassumption is that one need not pay tax as TDS has been deducted on the income. What people forget is that the tax deducted by the bank at source is at a flat rate of 10%. However, tax slabs may vary. So, if you fall in a higher tax slab, your liability may be more and you will have to pay the balance while filing returns. "Many people forget to re-calculate their liability and end up with a notice, paying higher taxes with interest and penalties," says Archit Gupta, Founder and CEO, ClearTax.com.

The department can catch such mistakes by matching your ITR with Form 26AS. The taxman also digs deeper, going beyond TDS. It tracks the deposits and interest income where TDS has not been deducted, that is, where you have submitted Form 15 G/H. The penalty is more severe (up to 200% of the tax evaded) as it is not a mis-calculation, but concealment of income.

2. Overlooking clubbing of income

Many people invest in the names of spouse or minor children. There is no limit to the amount you can give your spouse, but if you invest the gifted money, Section 64 of the Income Tax Act, a provision for clubbing income, comes into play. Under this, any earning from the gifted amount is added to your taxable income. "It doesn't matter if your spouse has an income or not. The money will be clubbed with your income," says Tapati Ghose, Partner, Deloitte Haskins & Sells LLP. For a minor child, the earning is treated as income of the parent who earns more. You also get an exemption of Rs 1,500 a year, per child, up to a maximum of two kids. If you want to escape tax, invest the gifted money in a tax-free option, such as the PPF or ELSS scheme. Or invest in the name of your parents or a major child, where clubbing provision does not come into play. Please click on the following link for Sec 64 of IT Act: "Clubbing of income under Income Tax Act 1961 with FAQ's"

3. Not filing returns

If you think you don't need to file returns because you don't have a tax liability, you are mistaken. This exemption is only for those with an annual gross income below the basic exemption level of Rs 2.5 lakh. Anyone with an income above this has to file a return. The basic exemption is Rs 2.5 lakh per year for people below 60 years, Rs 3 lakh for senior citizens above 60, and Rs 5 lakh for very senior citizens above 80. The rest, including NRIs, have to comply. If you fail to file your return in time, the assessing officer may levy a penalty of Rs 5,000 under Section 271F. Please click on the following links for Sec. 271F: "Penalty u/s 271F for belated returns"

Besides, the limits are for gross incomes, that is, the income before deductions and tax breaks. So, if your annual income is Rs 4 lakh and you invest Rs 1.5 under Section 80C, your tax liability will be zero. However, you are required to file your ITR. Similarly, if you have paid tax as TDS or advance tax, you will need to file the return.

Many salaried people, who earn less than Rs 5 lakh, don't file an ITR. The confusion is because of an ad hoc rule introduced in 2011-12, where salaried individuals with taxable incomes of Rs 5 lakh or less, and earning less than Rs 10,000 as interest from savings account, with no refund due, were exempt from filing returns. However, this rule has long been withdrawn.

4. Missing income from old job

Whether you received a single cheque from a part-time freelance assignment, or salary was credited regularly to your account, every single paisa has to be reported. If you fail to inform your current employer about a job change, there is a chance that lesser tax will be deducted from your salary than you are liable to pay. However, this discrepancy will be immediately reflected when you file your return. You may have to pay higher tax as duplicate benefits will be rolled back. Do not try to escape it as defaulters have to pay the balance tax along with interest at the rate of 1% per month for delay as penalty.

- Not reporting tax-free income

Tax-free does not mean it is not your income. All your earnings are included, be it the interest earned on PPF, tax-free bonds, or capital gains from stocks and gifts from specified relatives. "Even if you are not liable to pay any tax on these incomes, all your interest income has to be reported in the ITR," says Gupta. You can later claim exemption for it under various sections.

Source: Economic Times, http://www.incometaxindia.gov.in & Tax Guru.in

Source: Live Mint.

Can I just say what a comfort to uncover somebody that actually

knows what they are talking about online. You actually realize how to bring a problem to light and make it important.

A lot more people ought to read this and understand this side of the story.

I can’t believe you are not more popular since you surely have the gift.

Your look is unique in comparison to other people I’ve read stuff from.

Thanks a lot for posting when you’ve got an opportunity, Guess I’ll just bookmark this page.

Hey there! Would you mind if I share your blog with my facebook group?

There’s a lot of people that I think would really enjoy your content.

Please let me know. Cheers

Yes you may share . I hv no objection.

Yes! Finally someone writes about blogroll.

Nice Post, This Article is helpful to me

Thanks Mr Parag for your valuable comments. This motivates us in improving the contents of the website.

Thank you for the wonderful article. The content is thorough and easily understandable.

I have posted the latest Slabs for FY 2018-19 AY 2019-20. You may have a look at it.