Third Bi-monthly Monetary Policy Statement, 2019-20 Resolution of the Monetary Policy Committee (MPC) Reserve Bank of India

India's Central Bank Reserve Bank of India announced on 6th August the IIIrd Bi-Monthly Monetary Policy wherein they announced an array of conventional and unconventional measures to boost slowing economic growth, including reducing the benchmark interest rate by an irregular 35 basis points (bps), its fourth rate cut this year.

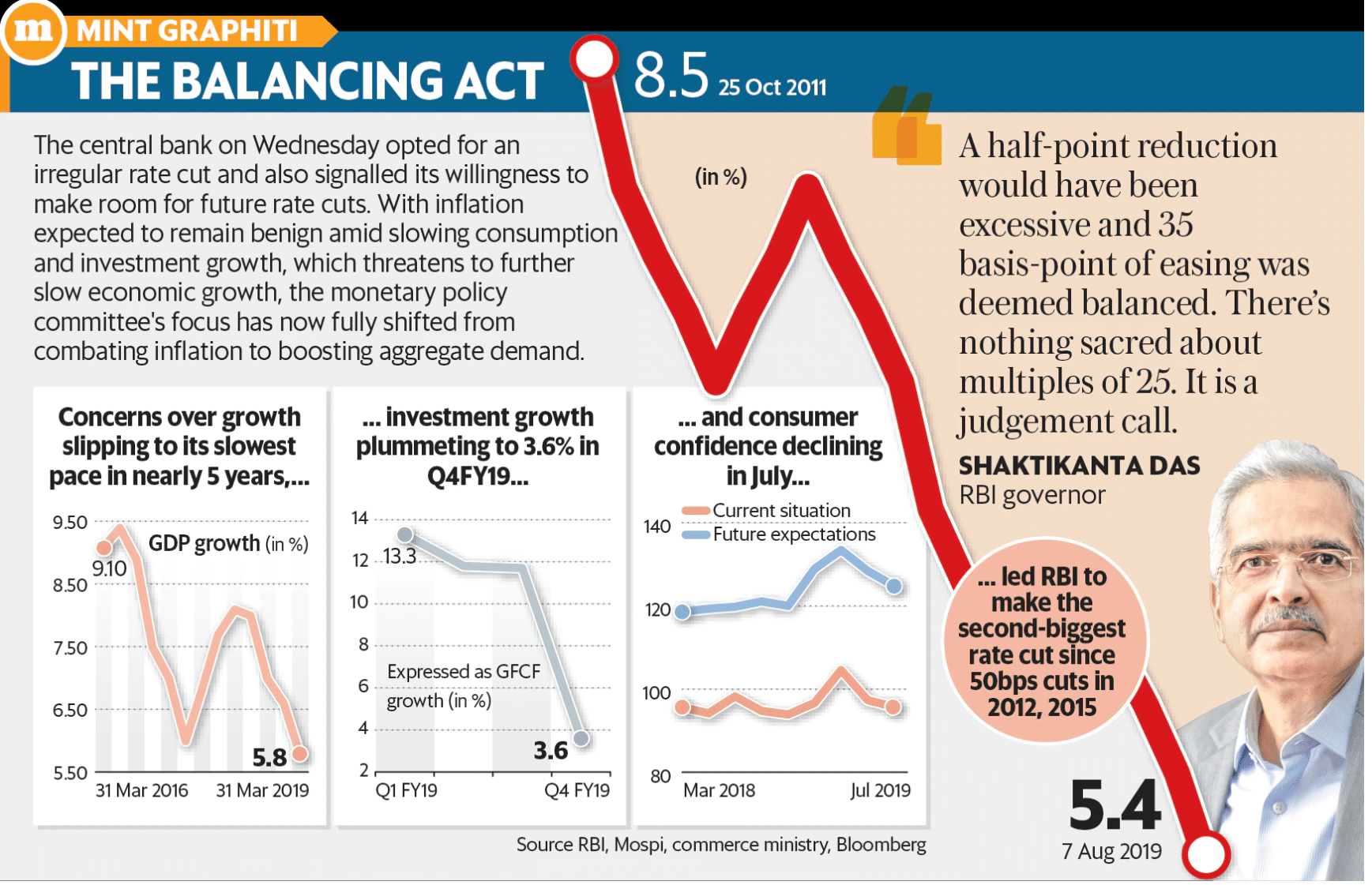

The Reserve Bank of India’s six-member rate-setting panel on Wednesday cut the repurchase rate to 5.4%, the lowest in almost a decade and more than the 25bps cut expected by most economists. It also decided to retain the monetary policy’s current accommodative stance.

Central bank governor Shaktikanta Das told reporters that the monetary policy committee (MPC) was of the view that the “standard 25 basis point (cut) might prove to be inadequate in view of the evolving global and domestic macroeconomic developments. On the other hand, reducing the rate by, say, 50 basis points might be excessive, especially after taking into account the actions already undertaken".

Reducing the rate by 35bps was, therefore, viewed as balanced, Das said. This is the second-biggest rate cut in recent times after RBI reduced the repo rate by 50bps twice: once in April 2012 and next in September 2015.

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today decided to:

- reduce the policy repo rate under the liquidity adjustment facility (LAF) by 35 basis points (bps) from 5.75 per cent to 5.40 per cent with immediate effect.

Consequently, the reverse repo rate under the LAF stands revised to 5.15 per cent, and the marginal standing facility (MSF) rate and the Bank Rate to 5.65 per cent.

- The MPC also decided to maintain the accommodative stance of monetary policy.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

The decision to cut rates by 35bps found support from four MPC members—Ravindra Dholakia, Michael Patra, B.P. Kanungo and governor Shaktikanta Das—while Pami Dua and Chetan Ghate voted for a 25bps reduction. All the members voted unanimously to maintain the monetary policy’s accommodative stance.

HIGHLIGHTS OF THIRD BI-MONTHLY POLICY

HIGHLIGHTS OF THIRD BI-MONTHLY POLICY

Following are the highlights of the third bi-monthly monetary policy announced by the RBI on Thursday:

* Repo rate reduced by 35 bps to 5.40 per cent for third time in a row

* Reverse repo rate now stands at 5.15 per cent, marginal standing facility (MSF) & Bank rate 5.65 per cent

* RBI maintains policy stance to accommodative.

* Cuts GDP growth forecast to 6.9 per cent from 7 per cent for FY20

* CPI inflation is projected at 3.1% for Q2 FY20 and 3.5-3.7% for H2 FY20.

- Charges on RTGS, NEFT transactions scrapped to promote digital transactions

** The next meeting of the MPC is scheduled during October 1, 3 and 4, 2019

Why RBI slashed repo rate by 35 bps instead of 25 or 50 bps ?

Quantum of rate cut a balanced call: In view of the current macro-economic condition assessed by the MPC members, a 25 bps rate cut would have been inadequate while a 50 bps cut would have been excessive, especially after taking into accounts actions already taken by RBI. Hence, a 35 bps rate cut was seen as a balanced call for now, explained RBI Governor Shaktikanta Das in a presser post policy announcement.

"The 35 bps rate cut should be seen as a signal that the RBI MPC is quite concerned with the growth outlook beyond the usual 25 bps rate cut in a business-as-usual scenario (even though it does not reflect in the revised FY2020 GDP growth estimate). The RBI MPC did not necessarily want to deliver a 50 bps rate cut and hence, retains the scope to reduce rates further," said Suvodeep Rakshit, Senior Economist at Kotak Institutional Equities.

"With inflation expected to remain benign, and further downside to growth outlook, we see scope for 25-50 bps of further rate cuts through FY2020," Rakshit added.

FY20 growth forecast lowered: Various high frequency indicators, the RBI said, suggested weakening of domestic and external demand conditions. This led the committee to lower GDP growth forecast for the financial year 2019-20 (FY20) to 6.9 per cent from 7 per cent, earlier. It observed that services sector activity for May-June present a mixed picture, while tractor and motorcycle sales – indicators of rural demand – continued to contract. Among indicators of urban demand, passenger vehicle sales contracted for the eighth consecutive month in June; however, domestic air passenger traffic growth turned positive in June after three consecutive months of contraction.

Global economy slows down: The MPC noted that global economic activity has slowed since the meeting of the MPC in June 2019, amidst elevated trade tensions and geo-political uncertainty. “GDP growth in the US decelerated in Q2:2019 while in the Euro area, too, GDP growth moderated during the period on worsening external conditions. Economic activity in the UK also continues to be subdued owing to Brexit-related uncertainty,” the RBI said.

Inflation outlook: The committee projected the CPI inflation at 3.1 per cent for the second quarter of the financial year 2019-20 (FY20) and 3.5-3.7 per cent for the second half of the fiscal year (H22019-20), with risks evenly balanced. CPI inflation for Q1 of 2020-21 is projected at 3.6 per cent.

Accommodative stance retained: The MPC also decided to maintain the accommodative stance of monetary policy. The stance means rate increase is off the table. In its June policy meet, the RBI had changed the stance to accommodative to neutral.

Liquidity concerns assuaged: The RBI, in its policy statement, noted that liquidity in the system was in large surplus in June-July 2019 due to factors such as return of currency to the banking system, reduction of excess cash reserve ratio (CRR) balances by banks, open market operation (OMO) purchase auctions, and the RBI’s foreign exchange market operations.

Transmission of rate cuts: The transmission of policy repo rate cuts on fresh rupee loans of banks has improved marginally since the last meeting of the MPC. Overall, banks reduced their WALR (weighted average lending rates) on fresh rupee loans by 29 bps during the current easing phase so far (February-June 2019), the statement added.

For full read on the "Statement by Governor Third Bi-Monthly Policy, 2019-20" please click on the following link: Statement by Governor - Third Bi-monthly Monetary Policy, 2019-20

Source: rbi.org.in, LivMint, Business Line , Business Standard & (Graphic: Sarvesh Kumar Sharma/Mint)