Account Aggregators System: New framework to access, Share financial Data

On September 2, 2021 the Reserve Bank of India’s (RBI) Account Aggregator (AA) Framework went live. Eight of India’s major banks — State Bank of India, ICICI Bank, Axis Bank, IDFC First Bank, Kotak Mahindra Bank, HDFC Bank, IndusInd Bank and Federal Bank — joined the Account Aggregator (AA) network that will enable customers to easily access and share their financial data. The framework, which has been under discussion since 2016 and in the testing phase for some time, will now be open to all customers.

On September 2, 2021 the Reserve Bank of India’s (RBI) Account Aggregator (AA) Framework went live. Eight of India’s major banks — State Bank of India, ICICI Bank, Axis Bank, IDFC First Bank, Kotak Mahindra Bank, HDFC Bank, IndusInd Bank and Federal Bank — joined the Account Aggregator (AA) network that will enable customers to easily access and share their financial data. The framework, which has been under discussion since 2016 and in the testing phase for some time, will now be open to all customers.

What is an Account Aggregator?

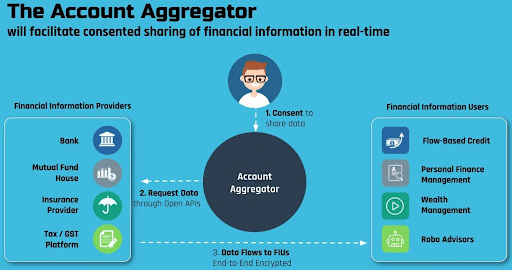

An account aggregator is a dashboard of all your financial data. You can then present this dashboard to any other entity whose services you need. Say, you want a loan. Your bank will want to check your monthly salary, income-tax returns, account statements and so on. All you need to do is to share your dashboard with the bank, instead having to share attested printouts of various documents.

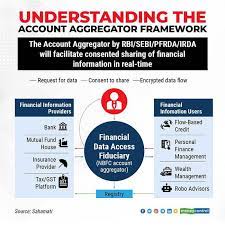

According to the Reserve Bank of India, an Account Aggregator is a non-banking financial company engaged in the business of providing, under a contract, the service of retrieving or collecting financial information pertaining to its customer. It is also engaged in consolidating, organising and presenting such information to the customer or any other financial information user as may be specified by the bank.

The AA framework was created through an inter-regulatory decision by RBI and other regulators including Securities and Exchange Board of India, Insurance Regulatory and Development Authority, and Pension Fund Regulatory and Development Authority (PFRDA) through and initiative of the Financial Stability and Development Council (FSDC). The licence for AAs is issued by the RBI, and the financial sector will have many AAs.

The AA framework allows customers to avail various financial services from a host of providers on a single portal based on a consent method, under which the consumers can choose what financial data to share and with which entity.

How does the system work?

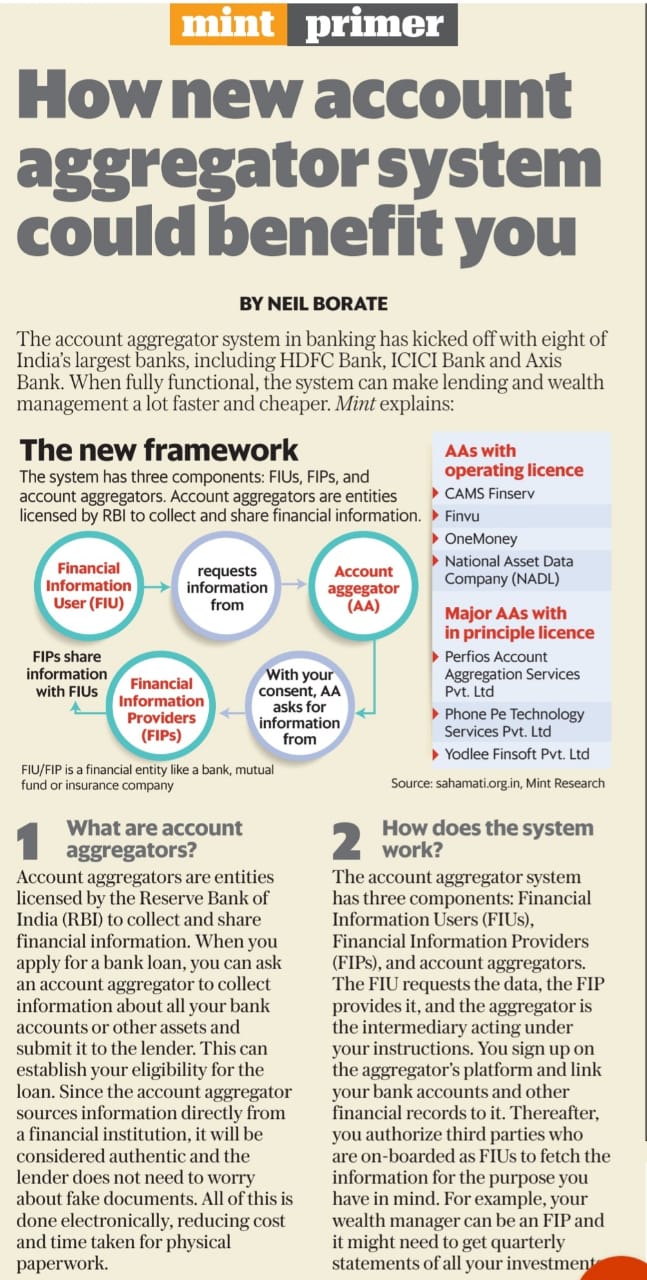

The account aggregator system has three components: Financial Information Users (FIUs), Financial Information Providers (FIPs), and account aggregators. The FIU requests the data, the FIP provides it, and the aggregator is the intermediary acting under your instructions. You sign up on the aggregator’s platform and link your bank accounts and other financial records to it.

The account aggregator system has three components: Financial Information Users (FIUs), Financial Information Providers (FIPs), and account aggregators. The FIU requests the data, the FIP provides it, and the aggregator is the intermediary acting under your instructions. You sign up on the aggregator’s platform and link your bank accounts and other financial records to it.

Thereafter, you authorize third parties who are on-boarded as FIUs to fetch the information for the purpose you have in mind. For example, your wealth manager can be an FIP and it might need to get quarterly statements of all your investments.

So far, CAMS FinServ, Cookiejar Technologies (product named Finvu), FinSec AA Solutions Private (OneMoney) and National E-Governance Services Asset Data are licensed as account aggregators. Three more – PhonePe, Perfios and Yodlee – have received in-principle approval.

What will the new system cost you?

The aggregator can either charge you or the FIU (data user) in question. The costs will be determined by each aggregator individually. However, due to the online nature of this system, they are likely to be low. In some cases, they might cut down on charges that you already have to bear when it comes to information verification. Take loan processing charges, for example.

What about privacy and consent?

The idea behind the new system is to enable you to give informed consent for data sharing. It will allow you to share specific information for a specific period. For example, you authorize the aggregator to share your bank account statement for a particular account for the last three years with a lender. The information being shared will be limited to that bank account and the time period mentioned. You will also have redressal options in case your information is shared without your consent.

Can an AA see or store data?

Data transmitted through the AA is encrypted. AAs are not allowed to store, process and sell the customer’s data. No financial information accessed by the AA from an FIP should reside with the AA. It should not use the services of a third-party service provider for undertaking the business of account aggregation. User authentication credentials of customers relating to accounts with various FIPs shall not be accessed by the AA, the RBI says.

Where is this system headed?

Although it is currently confined to areas under four regulators—RBI, Sebi, Irdai and PFRDA, talks are on to add more sources of information such as goods and service tax and income tax. These can help with areas like loan approval and wealth management. For instance, a tap of the finger could allow the aggregator to share your verified income tax returns with a bank which you have approached for a loan. Eventually, even documents like covid-19 vaccination certificates could become part of the system.

Source: Money Control.com; LiveMint