RBI’s Bi-Monthly Policy Review – Key Highlights

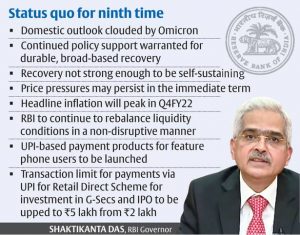

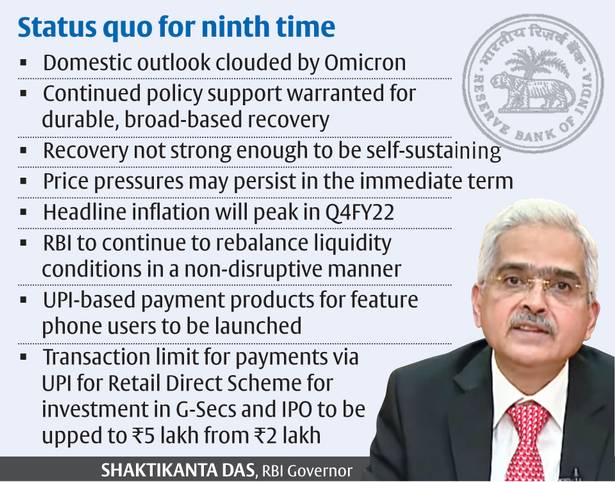

Reserve Bank of India (RBI) Governor Shaktikanta Das announced the policy decision on 8th December 2021, at the end of the scheduled review of the Monetary Policy Committee (MPC) that began on Wednesday, October 6. The MPC evaluated the economy at a time when there is a steady pick-up in activity and a calculated progress in the vaccination drive - with a quarter of India's adult population being fully vaccinated and almost 71 per cent partially vaccinated, amid the COVID-19 pandemic. The Reserve Bank of India's (RBI's) six-member monetary policy committee (MPC), headed by Governor Shaktikanta Das, decided to maintain key interest rates for a ninth straight meeting, retaining an accommodative stance amid the threat surrounding Omicron coronavirus variant.

Reserve Bank of India (RBI) Governor Shaktikanta Das announced the policy decision on 8th December 2021, at the end of the scheduled review of the Monetary Policy Committee (MPC) that began on Wednesday, October 6. The MPC evaluated the economy at a time when there is a steady pick-up in activity and a calculated progress in the vaccination drive - with a quarter of India's adult population being fully vaccinated and almost 71 per cent partially vaccinated, amid the COVID-19 pandemic. The Reserve Bank of India's (RBI's) six-member monetary policy committee (MPC), headed by Governor Shaktikanta Das, decided to maintain key interest rates for a ninth straight meeting, retaining an accommodative stance amid the threat surrounding Omicron coronavirus variant.

The Monetary Policy Committee (MPC) kept the repo rate unchanged at 4 per cent for the ninth consecutive time while maintaining an ‘accommodative stance’ as long as necessary, RBI Governor Shaktikanta Das announced on Wednesday.

The central bank governor said that the MPC had voted unanimously 5:1 to maintain the accommodative stance and added that the reverse repo rate too was kept unchanged at 3.35 per cent.

Following are the key Highlights of the Monetary Policy announcement:

- RBI keeps repo rate unchanged at 4 percent

- Reverse repo rate also remains unchanged at 3.35 percent.

- The MPC voted unanimously 5:1 to maintain 'accomodative' stance.

- The marginal standing facility (MSF) has also been left unchanged at 4.25 percent.

- Projection for real GDP growth is maintained at 9.5 percent. The central bank has however revised its Q3FY22 GDP growth to 6.6 percent from earlier 6.8 percent, and cut Q4FY22 GDP to 6 percent from 6.1 percent. Meanwhile, the RBI has cut Q4FY22 GDP to 6 percent from 6.1 percent earlier; and FY22 CPI inflation target has been maintained at 5.3 percent.

- FY22 CPI inflation target maintained at 5.3 percent. The October-December CPI inflation target has been revised to 5.1 percent from 4.5 percent earlier; while January-March CPI inflation forecast has been revised to 5.7 percent compared to 5.8 percent earlier.

- The Q1FY23 GDP growth forecast has been retained at 17.2 percent; Q2FY23 GDP growth seen at 7.8 percent; Q1FY23 CPI forecast revised to 5 percent from 5.2 percent; and Q2FY23 CPI forecast seen at 5 percent.

- From January 2022, liquidity adjustment will be mainly via the Variable Reverse Repo Auction. Headline CPI inflation is expected to peak in Q4 and soften thereafter.

- Proposed return to normal dispensation under MSF Window, as the “RBI remains committed to our ‘accommodative’ stance to broaden growth impulses”.

- Financial conditions turning increasingly volatile and there is considerable uncertainty over growth-inflation dynamics, thus RBI will continue to rebalance liquidity conditions in a non-disruptive manner.

- The aim is to re-establish 14-day Variable Reverse Repo Rate (VRRR) as the main liquidity operation. The RBI is to absorb Rs 6.5 lakh crore in VRRR auction on December 17 and absorb Rs 7.5 lakh crore in VRRR auction on December 31.

- RBI retains flexibility to fine-tune liquidity operations. It will allow banks to make one-time pre-payment with respect to TLTROs announced.

- RBI Governor Das says central bank would continue to manage liquidity in a manner to maintain financial stability

- Price stability remains cardinal principle of RBI as it fosters growth, stability: Governor Das while announcing monetary policy

- Govt consumption is also picking up from August, providing support to aggregate demand, said Das

- The RBI will release a discussion paper on charges on digital payments.

- It is to also launch Unified Payments Interface (UPI)-based Feature Phone Products.

- Further, UPI caps for gilts, retail and IPOs are to be enhanced to Rs 5 lakh

MPC noted that crude oil prices have eased, that consumption demand has been improving and rural demand is exhibiting resilience. Recovery in the Indian economy is gathering traction. Government consumption has picked up from October 2021.

"We hold strong buffer to manage global spillovers and inflation is broadly aligned with target. We are better prepared to deal with the invisible enemy – COVID-19. The domestic economic outlook is somewhat clouded by Omicron variant," said Governor Das.

Das said the recent tax cuts on petrol and diesel should help in crowding-in private investment. There has been significant deleveraging of corporate balance sheet. Government's focus on Capex should help in crowding-in private investment

Globally, economic activity levels are reaching pre-pandemic times, he believes.

Please click on the following link to read: Monetary Policy Statement, 2021-22 Resolution of the Monetary Policy Committee (MPC) December 6-8, 2021 ;

Please click on the following link to read the: Governor’s Statement: December 08, 2021

How economists and market experts reacted:

- Lakshmi Iyer, CIO – Debt & Head – Products, Kotak Mahindra Asset Management Company

In what seemed like a close call, the RBI MPC chose to maintain status quo on key benchmark rates. No material changes to growth and inflation forecasts too. This suggests RBIs caution on the recent developments on the pandemic front. While 14-day VRRR amount has been increased in a graded manner, there seems to be no sense of urgency on RBI’s part to initiate any abrupt liquidity drain out measures. Bond markets should draw comfort from this decision and continue to trade range bound. Global cues to dominate the rate moves going forward. - Dhaval Ajmera, Director of Ajmera Realty & Infra India

RBI maintaining status quo on rates augurs well for brining equilibrium in the demand-supply economics of the real estate industry. With low loan interest rate regime, the home sales velocity witnessed across key Indian cities will continue on upward trajectory. The stock markets are expected to remain buoyant and realty index will continue to advance with positive bias in the short to medium term.

The revision of GDP and inflation targets are seen to be milder than expectation. The upcoming discussion paper to make the digital payments more affordable is a positive take-away from Governor’s speech. The announcements related to digital payments can offer disruption and bring dynamism in financial inclusivity expedition in the country.