Lakshmi Vilas Bank Crisis – All you want to know about

The Lakshmi Vilas Bank Ltd. placed under Moratorium

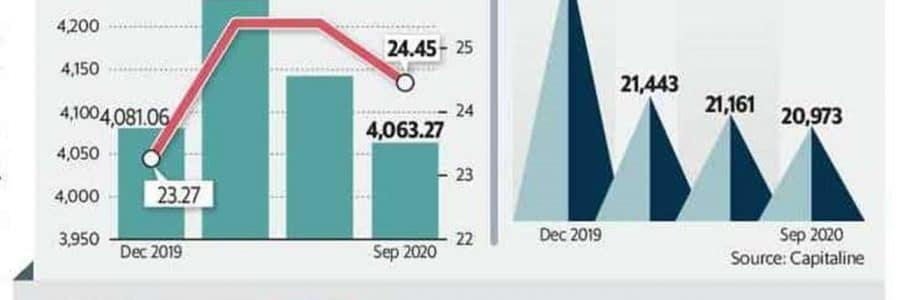

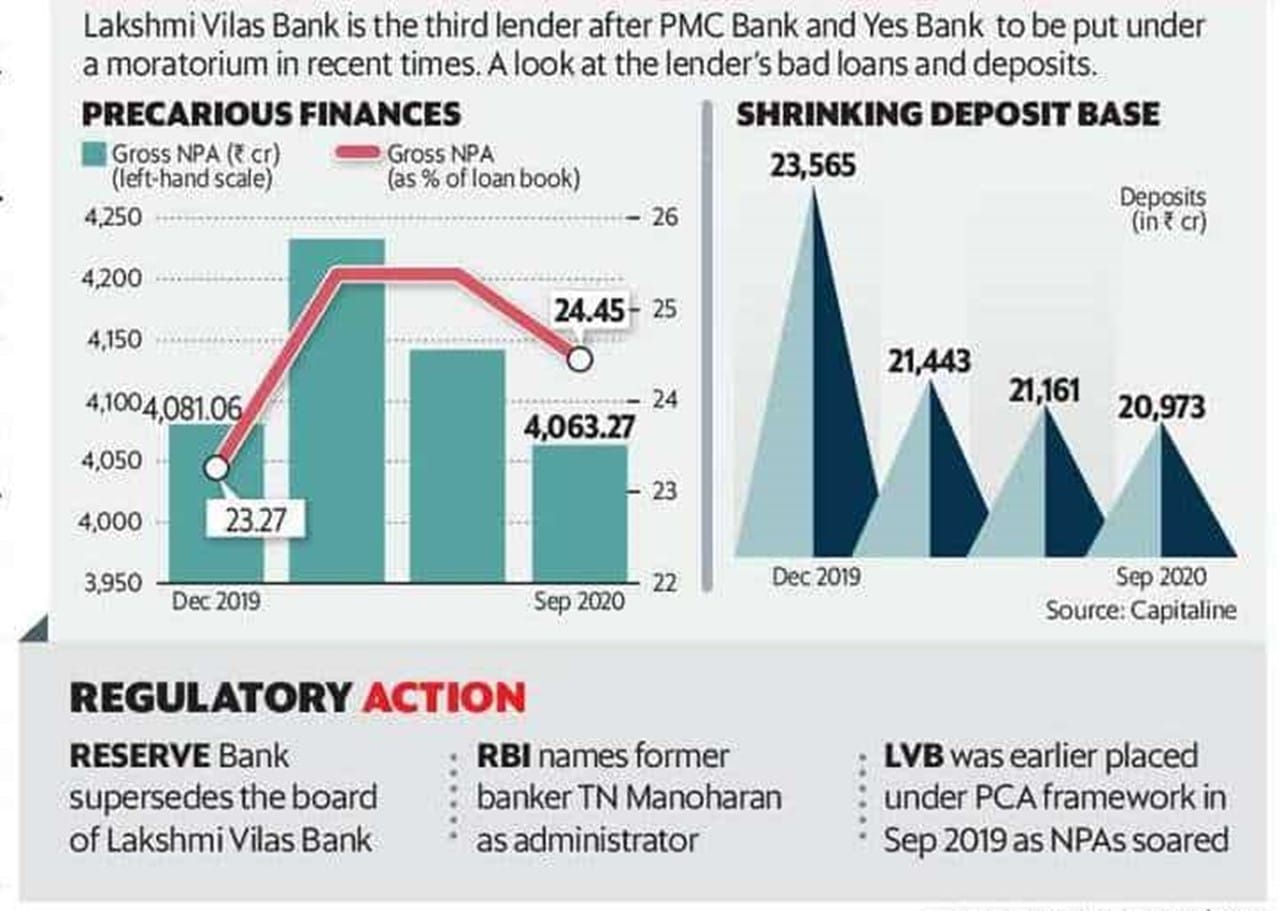

Lakshmi Vilas Bank is the third Bank after the PMC and Yes Bank to be placed under Moratorium in the recent times.

|

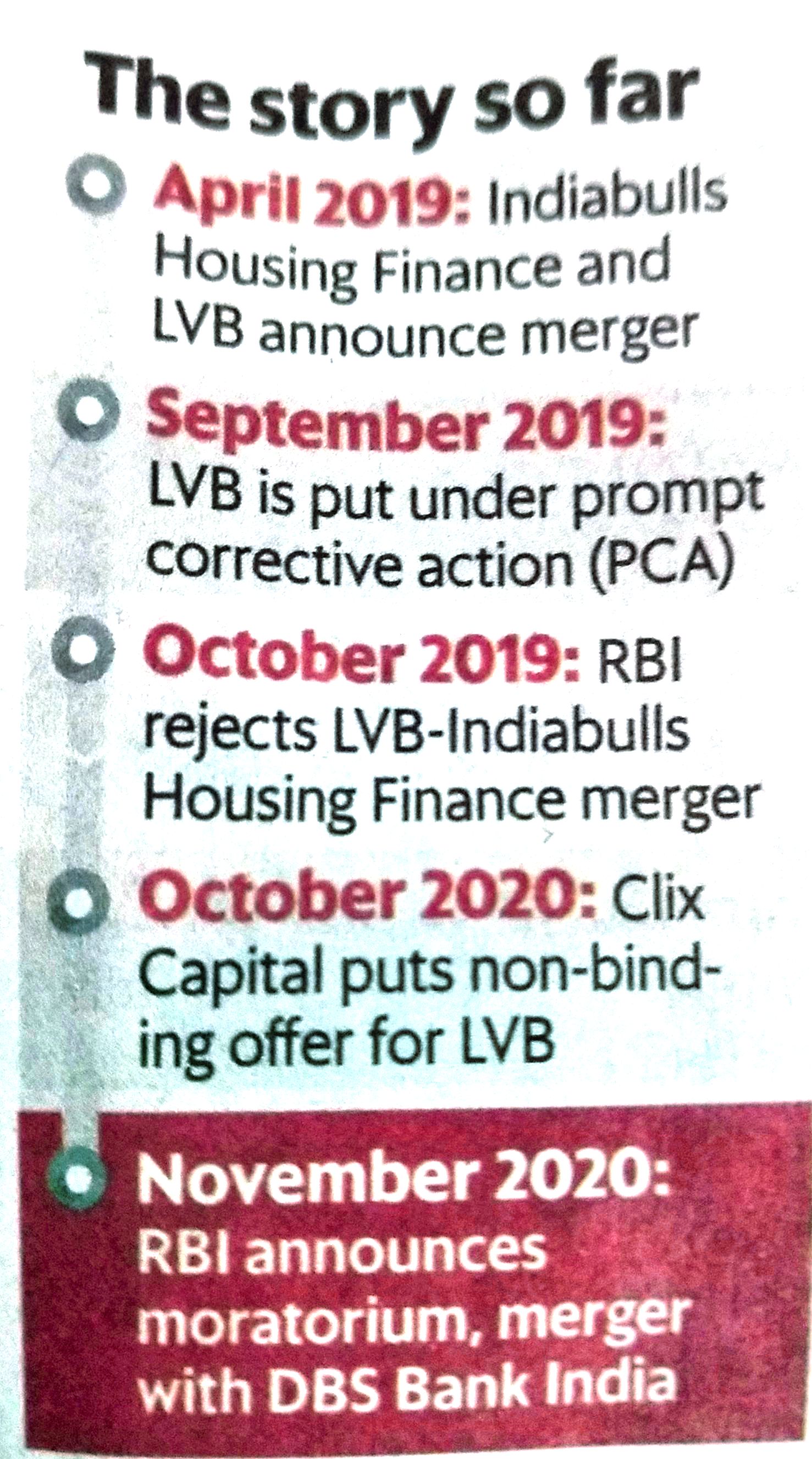

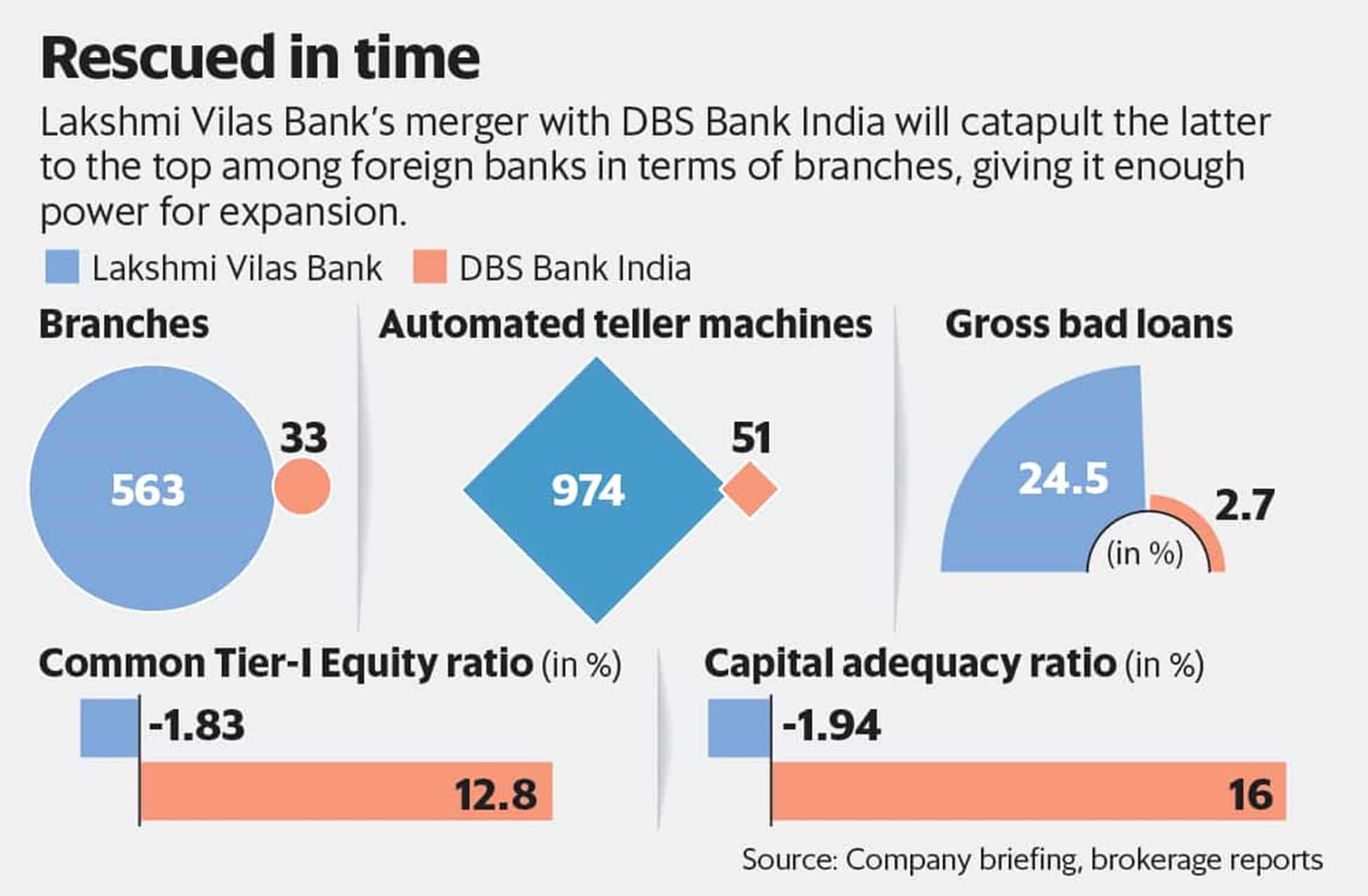

Moratorium on Lakshmi Vilas Bank, and what it means for depositors, financial sectorFailures of IL&FS, Punjab & Maharashtra Cooperative Bank and DHFL, and the bailout of Yes Bank, the Reserve Bank of India decision to impose a 30-day moratorium on Lakshmi Vilas Bank Ltd (LVB) and putting in place a draft scheme for its amalgamation with DBS Bank India, a subsidiary of DBS of Singapore, has raised concerns about the safety of the financial system. LV Bank was put under moratorium by RBI and is heading for amalgamation with DBS Bank India because the mounting NPA’s, Shrinking Deposit base and low level of liquidity plus the inability of the Management of LVB to bring in any adequate resolution plan and any suitable investor to bail out LVB. What about Safety of depositors and the financial system ? The RBI, which put a cap of Rs 25,000 on withdrawals, has assured depositors of the bank that their interest will be protected. The combined balance sheet of DBS India and LVB would remain healthy after the proposed amalgamation, with Capital to Risk Weighted Assets Ratio (CRAR) at 12.51% and Common Equity Tier-1 (CET-1) capital at 9.61%, without taking into account the infusion of additional capital. The RBI had earlier this year bailed out Yes Bank through a scheme backed by State Bank of India and other banks. One safety net for small depositors is the Deposit Insurance and Credit Guarantee Corporation (DICGC), an RBI subsidiary, which gives insurance cover on up to Rs 5 lakh deposits in banks. The RBI and the government have often assured that the financial system is safe and sound, but a spate of failures have the potential to affect the confidence of depositors. What has gone wrong with the sector? The collapse of IL&FS in 2018 had set off a chain reaction in the financial sector, leading to liquidity issues and defaults. Punjab & Maharashtra Co-op Bank was hit by a loan scam involving HDIL promoters and the bank is yet to be bailed out. The near-death experience of Yes Bank in March 2020 sent jitters among depositors. The RBI action against LVB was expected after shareholders recently voted against the appointment of seven directors to its board. Old-generation private banks had come under the spotlight, with shareholders of LVB and Dhanlaxmi Bank recently firing their chief executive officers in the span of a week. The LVB episode started unfolding after the RBI and banks led by SBI bailed out fraud-hit Yes Bank. The RBI has been monitoring the performance of private banks and large NBFCs. What happens to investors in these banks? Shareholders in Yes Bank faced a significant erosion in wealth as the stock price crashed below Rs 10 per share from a peak of Rs 400 per share. In the case of LVB, equity capital is being fully written off. This means existing shareholders face a total loss on their investments unless there are buyers in the secondary market who may ascribe some value to these. Shares of LVB closed at 20% lower circuit Wednesday. In its draft scheme for the amalgamation, the RBI said that “On and from the appointed date, the entire amount of the paid-up share capital and reserves and surplus, including the balances in the share/securities premium account of the transferor bank, shall stand written off.” In the case of Yes Bank, too, some individual investors faced a total loss on their investments in AT-1 bonds. Nearly Rs 9,000 crore worth of AT-1 bonds sold to various institutional investors, and to high net worth individual investors in the secondary market, were fully written off. As per RBI rules based on the Basel-III framework, AT-1 bonds have principal loss absorption features, which can cause a full write-down or conversion to equity What are the issues facing old-generation private banks? The functioning of many such banks has been under scrutiny in the last couple of years, as most of old-generation private banks do not have strong promoters, making them targets for mergers or forced amalgamation. Two other South-based banks – South Indian Bank and Federal Bank – have been operating as board-driven banks without a promoter. In Karur Vysya Bank, the promoter stake is 2.11%, and in Karnataka Bank, there’s no promoter. The problems in LVB follow the similar challenges faced by Yes Bank as well as Punjab & Maharashtra Co-operative Bank in recent times. What has been the regulatory response to these failures? On July 24, 2004, the RBI, then headed by Y V Reddy, announced a moratorium on private sector lender Global Trust Bank, which was then reeling under huge losses and bad loans. The bank was merged with public sector Oriental Bank of Commerce within 48 hours under an RBI-led rescue plan. Nearly 16 years later, the RBI has followed a somewhat similar approach on resuscitation of the troubled lenders of Yes Bank and now LVB. The moratorium announcement was followed by a reconstruction plan for Yes Bank and capital infusion by banks and financial institutions, with State Bank of India, ICICI Bank, Kotak Mahindra Bank, HDFC, Axis Bank and others putting in equity capital in the reconstructed entity. While banking observers agree that the RBI has acted whenever a bank or an NBFC faced trouble, the question remains whether it made the interventions swiftly. Will loan stress caused by the pandemic impact the banking system? NPAs in the banking sector are expected to increase as the pandemic affects cash flows of people and companies. However, the impact will differ depending upon the sector, as segments like pharmaceuticals and IT seem to have benefited in terms of revenues. NPA accretion in cash-rich sectors like IT, pharmaceuticals, FMCG, chemicals, automobiles is expected to be smaller when compared to areas like hospitality, tourism, aviation and other services. An expert committee headed by K V Kamath recently came out with recommendations on the financial parameters required for a one-time loan restructuring window for corporate borrowers under stress due to the pandemic. Corporate sector debt worth Rs 15.52 lakh crore has come under stress after Covid-19 hit India, while another Rs 22.20 lakh crore was already under stress. This effectively means Rs 37.72 crore (72% of the banking sector debt to industry) remains under stress. Companies in sectors such as retail trade, wholesale trade, roads and textiles are facing stress, while NBFCs, power, steel, real estate and construction were already under stress when the pandemic began. |

Things that depositors, shareholders and borrowers need to know

Depositor Issues

Depositors need not be worried with the moratorium on the LVB that restricts withdrawals. The Reserve Bank of India (RBI) has taken several measures to minimize issues that depositors could face due to the moratorium.

The RBI is also in the process of merging LVB with DBS Bank India, which has branded its banking services as digibank.

Depositors cannot withdraw over ₹25,000 across all their accounts. If an individual has a savings account and a fixed deposit, he can withdraw a total of ₹25,000 from both accounts. The restriction is per depositor and not per account.

The RBI has allowed up to ₹5 lakh withdrawal in cases of medical emergencies. The same applies if depositors want to pay fees for higher education for themselves or their dependents in India or abroad. Also, if there is marriage or other such function, a larger amount can be withdrawn.

Once the merger with DBS Bank India goes through, RBI would lift these restrictions. The interest accrued on deposits and balance in depositors’ accounts will be protected. DBS Bank India will pay the dues to depositors after the merger.

Following the merger, however, DBS Bank India could change the interest rates on existing deposits. So, keeping track of interest rates is important.

Going by previous mergers, an acquiring bank can change interest rates and terms and conditions.

LVB offers 3.25% interest rate on savings of up to ₹1 lakh. DBS Bank India, on the other hand, offers 3.5% interest rates on the same.

LVB’s rate is fix at 6% for fixed deposits of one- and 10 year tenure. DBS Bank's rates on FDs are lower. It offers 4.05% on one-year FD, 4.3% on two-year FD, 5.5% on deposits over three years.

Customers should Stop all auto-credits into LVB savings account

If a customer’s salary or any other income such as dividends on shares etc was being auto-credited into his LVB savings account then immediately inform the payer to route the credits to an alternative savings account of yours. If the customer doesn't have another savings account then he need to open one with a well-established, large, financially stable bank.

Customer should inform the payer of these incomes in writing that the payments be credited into a different bank savings account i.e. change the earlier bank mandate given to the payer. Once LVB-DBS merger is complete, then evaluate whether you want to continue your existing LVB savings account (post its merger with DBS) and restart the credits into the account.

Regarding auto-debit from LVB accounts during the moratorium period

If the customer has given mandates for auto-debit of mutual fund SIPs, loan EMIs, insurance premium payments etc., from LVB account then these payments will be debited from LVB account provided the total amount of debits does not exceed Rs 25,000 during the moratorium period. If the total amount exceeds Rs 25,000, then customer may face issues. Therefore, customer should request the financial institution which is receiving the auto-debit money to accept alternative payment mechanism. Ask if the auto-debit during the LVB moratorium can be avoided.

Further, the RBI has clarified that if a depositor has taken a loan from LVB whose EMI due date falls during the moratorium period, then such EMIs will be debited from the depositor's account. Remaining balance in account, if any, will be available for withdrawal purposes. For instance, assuming that the EMI of LVB loan is Rs 13,000 and EMI debit date is 25 of every month from LVB account, the customer will be eligible to withdraw Rs 12,000 only (Rs 25,000 - Rs 13,000) during the moratorium period.

IFSC code: Another thing to keep in mind is that post the merger, the IFSC codes will also change. This means that customers who wish to continue their accounts with the merged entity, will have to register new bank mandates wherever they have used the IFSC code for auto-debit purposes; this could be with mutual fund houses, insurance companies, NPS deposits etc.

Shareholders' Issues - LVB shareholders will get nothing after merger with DBS-LVB’s shares will be delisted from stock exchanges.

According to the draft scheme of amalgamation, the entire paid-up share capital of the LVB will be wiped out. “As it appears in the draft scheme, the value of the equity capital will be zero,"All shareholders are wiped out, and the shares will go to zero.”

(No DBS bank shares are given as compensation)," according to a note from Capitalmind, a Bengaluru-based investment research company. If you are a shareholder of LVB, the value of your shares will be zero.

The note also said that Tier-2 bondholders “seem to be fully protected". It means DBS Bank India will not write-downs the Tier-2 bonds. In Yes Bank’s case, Tier-2 bonds were written down. Some investors had approached courts against this move.

Borrowers' Issues

There are restrictions on payments that the bank must make. There are no restrictions on the money that the bank has to receive from borrowers. For those who have an ongoing loan with LVB, they will need to continue repaying their equated monthly installments (EMI) as usual.

There is a possibility that the interest rates, especially on floating-rate loans, could change once the merger comes through. Borrowers, therefore, need to keep track of interest rate changes on their loans.

DBS Bank India offers only limited loan products. For some loans, like home loans, it has partnered with housing finance companies.

If you are among borrowers who recently repaid a loan, you can approach the bank to release the mortgage or hypothecation. The government has allowed the bank to release pledged securities, mortgages, hypothecations, etc., in cases where the bank has received the entire payment.

RBI has protected the depositors and bondholders but wiped out the shareholders’ investment value. Shareholders are part owner in a company. They reap benefits when the company profits and thus must bear the brunt when the business is making losses.

Credit Rating Agencies Views:

Moody's Investors Service on Wednesday said Singapore's DBS Bank will strengthen its India business following merger with troubled Lakshmi Vilas Bank. The acquisition will help DBS complement traditional physical branch banking with its digital strategy in India.

Moody's said LVB's rescue process highlights the deficiencies in India's bank resolution mechanism as the moratorium restricts full and timely payments to depositors and creditors, thereby leading to a temporary default by the bank. This is despite the fact that the Indian government recently gave powers to the RBI to resolve a bank without imposing a moratorium.

S&P Global Ratings on Thursday said the Reserve Bank of India's swift resolution of troubled Lakshmi Vilas Bank will keep contagion at bay and help maintain stability in the banking system. S&P said this deal is positive for India's banking sector and will bring much-needed relief to LVB, which has been struggling for many years.

The US-based rating agency said it has always viewed the Indian government as highly supportive of the banking sector as it has consistently supported weak commercial banks by promoting the merger of distressed institutions with stronger lenders.

It has historically not allowed commercial banks to fail and has swiftly stepped in to address trouble. In this case also, the RBI and the government stepped quickly to prevent any loss to the creditors, including depositors, and maintain system stability.

"In our view, the RBI's decision to consider a foreign bank, beyond just homegrown institutions, to bail out LVB demonstrates its willingness to put control of banking assets in foreign entities," S&P said.

(Source: rbi.org.in, Money Control, Live Mint, Economic Times, Hindustan Times & Indian Express)